The Bitcoin Iran deal rally on renewed U.S.-Iran deal optimism is a credible first-order macro signal. The move still needs confirmation in oil flows, gasoline prices, inflation compensation, and Fed pricing before traders can treat it as a reopened path to rate cuts.

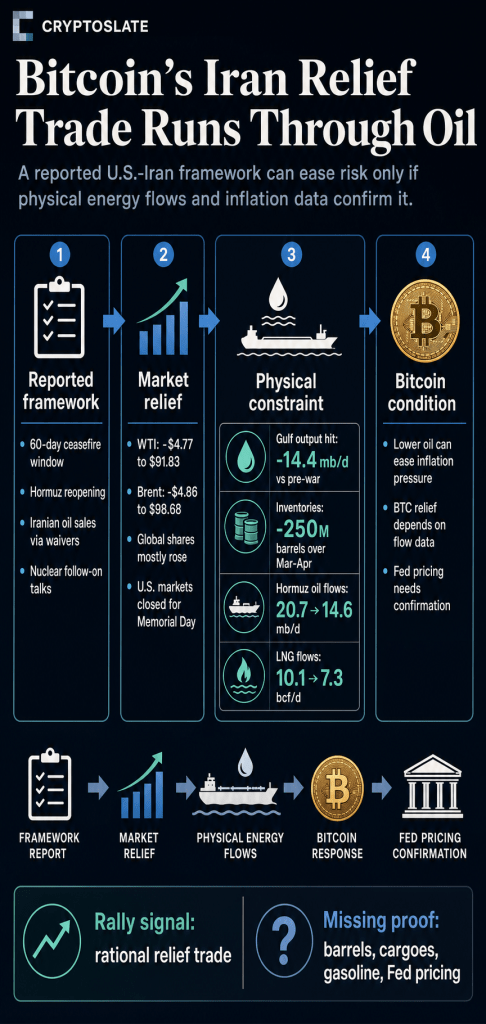

The immediate market logic is straightforward. A reported framework could extend the ceasefire for 60 days, reopen the Strait of Hormuz, allow Iranian oil sales through sanctions waivers, and move nuclear concessions into follow-on negotiations.

If that sequence holds, the war premium in crude can fall. Gasoline pressure can ease, inflation readings can cool, Treasury yields can soften, and Bitcoin can trade less like an asset trapped under real-rate pressure.

The bounce is therefore as much a liquidity signal as a geopolitical one. BTC traded between $77,400 and $77,500 on May 25, still far below its October 2025 high of $126,198.

In that context, any signal that pulls the market away from higher oil prices and a tougher Fed policy can trigger an outsized relief move.

The stronger interpretation is that markets are paying up front for a deal whose value depends on as-yet-unsettled facts: physical shipping through the Hormuz Strait, oil and LNG flows, gasoline pass-through, inflation compensation, Fed communication, and durable nuclear limits.

Oil is the first Bitcoin Iran deal rally test

The fastest transmission channel from the reported deal to Bitcoin runs through crude. Global shares mostly rose while WTI crude fell $4.77 to $91.83 and Brent fell $4.86 to $98.68 after President Donald Trump said Iran talks were progressing.

U.S. markets were closed for Memorial Day, so the move is best read as a global-market and oil-futures reaction rather than a full U.S. risk-asset close. Even with that caveat, the direction was clear: lower oil, less immediate inflation pressure, and more room for risk assets to recover.

The reported deal terms explain the move. The draft framework would extend the ceasefire, reopen Hormuz, allow Iran to sell oil, and begin negotiations over curbing Iran’s nuclear program.

A similar outline described a gradual reopening of the waterway, sanctions waivers for oil sales, and unresolved details around enrichment and nuclear material.

For Bitcoin, the oil channel is central to the trade. The asset has spent much of the Iran war period behaving like a liquidity-sensitive risk asset, under pressure from higher energy costs and tighter Fed pricing.

A credible reduction in the oil shock can support crypto by lowering the probability that policymakers need to keep policy restrictive for longer, or respond to a renewed inflation pulse with a more hawkish stance.

That makes the relief rally rational and conditional. The first move in crude signals to traders that the geopolitical premium can unwind quickly when the market sees a path to the reopening of Hormuz.

The second move has to come from physical energy data and inflation readings. Without those, the rally remains a bet on implementation rather than a confirmed macro turn.

That distinction keeps the market signal anchored in data. Bitcoin can react immediately to futures pricing, but the Fed will need evidence from energy flows and inflation indicators before treating the shock as temporary.

Hormuz relief needs physical normalization

The physical energy backdrop remains large enough that a diplomatic outline still has to become a functioning oil market.

The International Energy Agency said Gulf output affected by the Hormuz closure was 14.4 million barrels per day below pre-war levels, while observed global inventories drew by about 250 million barrels over March and April.

The U.S. Energy Information Administration’s chokepoint data showed oil flows through the Strait of Hormuz falling from 20.7 million barrels per day in the fourth quarter of 2025 to 14.6 million barrels per day in the first quarter of 2026.

LNG flows fell from 10.1 billion cubic feet per day to 7.3 billion over the same period.

Those numbers explain why reopening Hormuz would register immediately across risk assets. They also show the scale of the implementation gap.

Oil and LNG flows, Gulf production, and inventories have to move back toward normal before lower futures prices become a durable disinflation signal.

| Relief signal | Why it helps Bitcoin | What still has to resolve |

|---|---|---|

| Ceasefire extension and Hormuz reopening | Reduces the immediate oil-risk premium and supports risk assets | Oil and LNG flows have to recover in actual data |

| Iranian oil sales under waivers | Adds potential supply and lowers pressure on crude futures | Exports, sanctions mechanics, and regional security terms remain implementation risks |

| Nuclear follow-on talks | Could reduce the geopolitical premium if concessions are verifiable | Enrichment limits, uranium removal, inspections, and duration remain unresolved |

| Lower oil and gasoline pressure | Can ease inflation and real-rate pressure on crypto | April inflation data already show a large energy pass-through that has to reverse |

The positive case is clear: reopening Hormuz and restoring oil flows would lower the inflation impulse that has been weighing on liquidity expectations.

The unresolved case is equally important: a slow recovery in flows, persistent disruption in Gulf production, or elevated gasoline prices would leave the Fed with less room to validate the market’s relief trade.

The Bitcoin Iran deal rally runs through the Fed rate-cut path

Bitcoin is rallying because de-escalation can change the rate conversation through energy prices. A cooler energy market can pull inflation readings and inflation compensation away from the worst Iran-war scenarios, making the Fed less likely to delay cuts further or keep the risk of a hike alive.

The April inflation data explain the sensitivity. The Bureau of Labor Statistics said CPI rose 0.6% month over month and 3.8% year over year, while energy rose 17.9% and gasoline jumped 28.4% over 12 months.

That is the kind of pass-through that turns foreign-policy shocks into domestic rate pressure.

The Fed had already reacted to that backdrop. Its April statement held the federal funds target range at 3.50% to 3.75%, cited elevated inflation partly reflecting global energy prices, and showed internal tension around easing language.

Minutes from the April meeting said expected cuts had shifted later into the third and fourth quarters of 2026 and the first quarter of 2027, while options pricing implied about a 30% probability of a rate hike by the first quarter of 2027.

That last point is the core Bitcoin problem. Crypto can absorb a geopolitical shock more easily if the shock lowers rates or brings liquidity back into view.

It struggles when the same shock raises oil, lifts inflation compensation, keeps yields high, and delays cuts. The recent Fed minutes backdrop already turned the market’s worst macro twist into a move from pricing cuts to pricing some risk of hikes.

A U.S.-Iran deal can reverse that pressure only if it changes the inflation data and market-implied inflation path. Lower crude futures help. Lower gasoline prices help more.

A decline in breakeven inflation and a softer Fed communication path would be the strongest signals that the central bank can look through the oil shock before the 2026 midterms.

That sequence is why Bitcoin’s move should be read as a conditional rates trade. The asset can rebound before every geopolitical question is settled. It still needs sufficient energy relief to shift the inflation-versus-Fed-pricing balance away from the hike-risk scenario that dominated after the April minutes.

Durable nuclear limits decide how long oil relief lasts

The political fight over whether the reported framework is stronger than the Obama-era Joint Comprehensive Plan of Action has a direct market consequence: the durability of the oil-risk premium.

The strongest defensible answer is specific. The reported framework could be stronger than the JCPOA on one crucial point if Iran verifiably gives up roughly 440.9 kilograms of uranium enriched up to 60%.

That would directly address a near-weapons-grade stockpile that did not exist in the same form when the original JCPOA was negotiated.

The reported framework remains incomplete as an overall comparison. The JCPOA capped Iran’s enrichment at 3.67% for 15 years, kept its enriched uranium stockpile below 300 kilograms of 3.67% material, restricted centrifuges, limited activity at Fordow, and included monitoring and dispute mechanisms involving the International Atomic Energy Agency and a Joint Commission.

The Obama White House framed the agreement as cutting Iran’s uranium stockpile by 98% and extending breakout time. The Council on Foreign Relations notes that Trump later withdrew the U.S. after criticizing the pact as insufficient.

That benchmark makes the current comparison concrete. A verified handoff or dilution of 60% uranium would be a meaningful concession.

A pledge never to pursue nuclear weapons is also politically important. Yet if enrichment suspension, long-term caps, verification access, duration, and Fordow restrictions remain open or absent, the market lacks a firm basis for saying the new framework has removed the risk that pushed oil higher.

That is where the Bitcoin rally and the political debate meet. If the final text looks like a ceasefire plus deferred nuclear talks, immediate oil relief could still fade into another risk premium.

If it pairs Hormuz normalization with verifiable uranium removal and enforceable limits, it gives the Fed a better chance to treat the shock as temporary.

The data test comes next

The Bitcoin Iran deal rally is credible as a relief trade and premature as a full macro verdict.

The bullish version is easy to map. Tankers return. Iranian oil sales add supply. Brent and WTI keep falling. Gasoline prices follow. Breakeven inflation cools.

Treasury yields no longer carry an oil-shock premium. Fed officials regain confidence that energy pressure will not contaminate inflation expectations. In that world, the market can bring forward the timing of rate cuts, and Bitcoin’s rebound can become more than a geopolitical headline trade.

The bearish version requires only enough unresolved risk for energy markets to keep pricing disruption. If Hormuz flows remain impaired, if Gulf production remains constrained, if gasoline stays high, or if the final nuclear language looks weaker than the JCPOA on enrichment and verification, the Fed and midterm voters face much the same inflation problem under a calmer label.

That is the test. Bitcoin is right to respond to lower oil pressure because the rate channel is real.

Traders would overreach if they treated a reported political framework as already equivalent to disinflation. The rally becomes a durable macro off-ramp when the deal shows up in barrels, cargoes, gas stations, inflation compensation, and Fed pricing before November 2026.

Until then, the Bitcoin Iran deal rally is a rational relief trade waiting for proof in the data.

The post Bitcoin Iran-deal rally faces its real test in oil flows and Fed pricing appeared first on CryptoSlate.